Getting a letter from the IRS is stressful.

Many people put it aside because they do not know what it means. That is a mistake. IRS collection follows a process, and each notice matters.

If you owe back taxes, the notice sequence can lead to liens, levies, wage garnishment, and appeals deadlines.

The earlier you act, the more options you keep.

Contributor insight: Christopher Nichols, Director of Tax Resolution at Badran Tax, spent 24 years at the IRS. He served as a Revenue Officer for 20 years and later worked in the Independent Office of Appeals as a Settlement Officer. He now helps taxpayers resolve IRS collection matters in private practice.

How IRS Collection Starts

After You File Your Tax Return and Do Not Pay

If you file a tax return and do not pay the full balance, the IRS sends a bill. That bill starts the collection process.

The IRS explains this in Topic No. 201, The Collection Process and Publication 594, The IRS Collection Process.

Quick summary:

- The first IRS bill starts the collection process.

- Penalties and interest keep growing until the balance is resolved.

- Ignoring notices increases both cost and enforcement risk.

The Notice Cycle

Most taxpayers first receive a CP14 notice. After that, the IRS may send follow-up notices such as CP501, CP503, and CP504.

Each letter becomes more urgent. They are warnings, not background noise.

What CP504 Means

CP504 is serious, but it is often misunderstood.

It warns of levy action and can allow levy in limited situations, such as certain state tax refunds. But CP504 is usually not the formal notice that gives full Collection Due Process rights before most levy action.

The IRS explains this in its Collection Due Process FAQs.

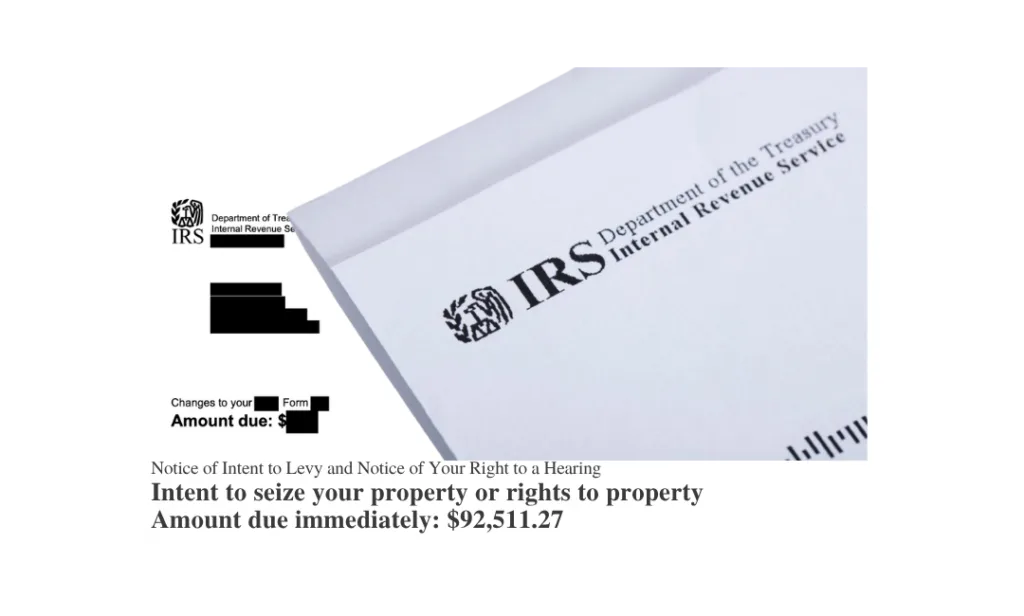

Final Notice of Intent to Levy

The Most Important IRS Notice to Review

The most important collection notice is usually the Final Notice of Intent to Levy and Notice of Your Right to a Hearing, often issued as Letter 1058 or LT11.

This is the notice that triggers your right to request a Collection Due Process (CDP) hearing.

Why this letter matters:

- You generally have 30 days from the notice date to request a CDP hearing.

- A timely request can stop most levy action while Appeals reviews the case.

- A timely request can preserve your right to seek Tax Court review later.

The Taxpayer Advocate Service explains CDP rights here: Collection Due Process (CDP).

You can request a CDP or equivalent hearing using Form 12153.

Your Main Options During a CDP Hearing

If you respond within the 30-day window, Appeals can review collection alternatives that fit your situation.

- Installment Agreement: A monthly payment plan.

- Offer in Compromise: A request to settle for less than the full amount if you qualify.

- Currently Not Collectible (CNC): A hardship status if paying would prevent you from covering necessary living expenses.

- Penalty relief: Possible in some cases, depending on the facts.

Publication 1660 explains these rights in more detail: Publication 1660, Collection Appeal Rights.

What Appeals Reviews

Appeals looks at your income, expenses, assets, account history, and whether the IRS followed the required procedures.

Clear documentation matters. Weak or missing records make relief harder to obtain.

What Happens If You Miss the 30-Day Deadline

Missing the deadline is a major setback, but it does not always end your options.

You may still request an equivalent hearing within one year of the notice date.

But an equivalent hearing is not the same as a timely CDP hearing.

- You usually do not preserve Tax Court review rights.

- Collection is not protected the same way.

- The IRS may already be in a stronger enforcement position.

The Taxpayer Advocate Service explains equivalent hearings here: Equivalent Hearing (Within 1 Year).

How the 10-Year Collection Rule Works

Federal tax debt does not last forever.

In general, the IRS has 10 years from the assessment date to collect a tax debt. This is often called the collection statute expiration date, or CSED.

But some events can pause that 10-year period. Timely CDP requests, some appeals, bankruptcy, and pending Offers in Compromise can extend the time the IRS has to collect.

The IRS discusses collection timing here: Collection process for taxpayers filing and or paying late.

How Penalties and Interest Grow

Once a balance is assessed, penalties and interest begin to add up.

Interest generally continues until the balance is paid in full or otherwise resolved. An installment agreement does not stop interest.

However, for eligible individuals who filed on time, an approved installment agreement can reduce the failure-to-pay penalty rate while the agreement is in effect.

The IRS explains this here: Failure to Pay Penalty.

Can You File an Offer in Compromise During Collection?

Yes. An Offer in Compromise (OIC) can be raised as a collection alternative during the CDP process if it fits your situation.

The IRS includes OIC information on Form 12153 and explains the program here: Offer in Compromise FAQs.

That said, an OIC is documentation-heavy. It requires a full financial disclosure and a sound strategy. Filing one carelessly can waste time and weaken your position.

What If You Never Filed the Return?

Collection can become worse when the return was never filed.

If you do not file, the IRS may prepare a substitute for return. That return often does not include deductions, credits, or exemptions you may have claimed yourself.

The IRS explains that process here: Filing past due tax returns.

Even if you cannot pay, filing your own return is usually much better than letting the IRS file one for you.

Common Mistakes Taxpayers Make

- Ignoring early notices because they do not look final

- Missing the 30-day CDP deadline

- Assuming CP504 is the last letter that matters

- Waiting until a levy hits a bank account or paycheck

- Filing an Offer in Compromise without full financial support

- Failing to update the IRS with a current mailing address

The IRS generally only needs to mail notices to your last known address. If you moved and did not update your records, that can create major problems.

When to Get Professional Help

If you received a final levy notice, already face wage garnishment or bank levy risk, or need to propose a collection alternative, this is usually the point where professional help matters most.

Badran Tax focuses on tax debt reduction and IRS problem resolution.

If you are dealing with collection notices, wage garnishment, bank levy exposure, or long-standing tax debt, early intervention can protect your rights and expand your options.

Schedule a confidential consultation:

BadranTax Tax Consultation

Helpful Resources

- IRS Publication 594 – The IRS Collection Process

- IRS Publication 1660 – Collection Appeal Rights

- IRS Form 12153 – Request for a Collection Due Process or Equivalent Hearing

- IRS – Failure to Pay Penalty

- IRS – Offer in Compromise FAQs

- Taxpayer Advocate Service – Collection Due Process

Frequently Asked Questions (FAQ)

What is the first IRS collection notice after I file and owe?

For many taxpayers, the first balance-due notice is CP14. It starts the collection process and shows the amount due, plus penalties and interest if applicable.

Does CP504 mean the IRS can immediately levy my bank account?

CP504 is serious, but it is not usually the formal CDP levy notice for most levy action. The IRS generally must still issue a formal Final Notice of Intent to Levy and Notice of Your Right to a Hearing before most levy action begins.

What is the 30-day deadline on the final levy notice?

That is generally the deadline to request a Collection Due Process hearing using Form 12153. A timely request can protect your appeal rights and usually stops most levy action while Appeals reviews the case.

What happens if I miss the 30-day CDP deadline?

You may still request an equivalent hearing within one year, but you usually lose Tax Court review rights and do not receive the same level of protection from collection action.

Can I ask for an installment agreement during the collection process?

Yes. An installment agreement is one of the main collection alternatives the IRS and Appeals can consider.

Does an installment agreement stop interest?

No. Interest generally continues to accrue. However, for eligible individuals who filed on time, the failure-to-pay penalty rate can be reduced while an approved installment agreement is in effect.

Can I settle my tax debt for less than I owe?

Possibly. An Offer in Compromise may be available if your financial situation supports it. Qualification is strict and requires full financial disclosure.

What if I never filed the return?

The IRS may file a substitute for return, which often produces a higher tax bill because it may not include deductions or credits you could have claimed.

Can IRS tax debt hurt my credit?

Federal tax liens no longer appear on standard consumer credit reports, but a filed federal tax lien is still a public record and can still affect borrowing and lender review.

Can the IRS collect from retirement accounts?

In some cases, yes. The IRS has broad levy powers, although retirement accounts are not usually the first target. Waiting until enforcement reaches that stage is risky.

Does bankruptcy stop IRS collection?

Bankruptcy can affect collection, but tax debt treatment in bankruptcy is very fact-specific. Some taxes may remain collectible.

Are both spouses liable on a joint return?

Usually, yes. A joint return generally creates joint and several liability. In some cases, innocent spouse relief or related relief may be available.

Bottom Line

IRS collection does not start with a levy. It starts with notices.

Those notices build toward deadlines, appeal rights, and enforcement action. The earlier you respond, the more control you keep.

If you receive a final levy notice, do not treat it like routine mail. That 30-day window can be the difference between preserving your rights and reacting after enforcement has already started.

Amro Badran, EA is the Managing Partner of BadranTax LLC,

Experienced and Trusted Tax Resolution Firm based in New Brunswick, NJ.

With over 40 years of experience and accreditation as a Federal Enrolled Agent, Amro Badran and his team of experts specialize in helping individuals and businesses resolve complex IRS issues and controversies.

Disclaimer

This blog post is provided for educational and informational purposes only.

It does not constitute tax, legal, accounting, or financial advice and should not be relied upon as a substitute for professional counseling tailored to your specific situation.

Always consult a qualified tax advisor or legal professional before making decisions based on this content.

Use of this site or information herein does not create a professional relationship between you and BadranTax LLC or its principals. Any reliance on the material is solely at your own risk.

While we strive to provide accurate, up-to-date information, BadranTax makes no warranties, express or implied, regarding accuracy, completeness, or suitability of the content.

Links to external websites are provided for convenience only. BadranTax does not endorse and is not responsible for the content or practices of third-party sites.

BadranTax and its affiliates expressly disclaim all liability for any actions taken or not taken based on this information.