Tax debt is one of the most common financial issues Americans face, yet it’s often misunderstood.

Many people know they “owe the IRS,” but they are unsure what that actually means, how it started, or what happens next. Tax debt doesn’t usually appear overnight. It builds quietly through unpaid balances, missed filings, or unexpected tax bills, then grows as penalties and interest are added.

This article explains what tax debt is, how it happens, why it grows, and what taxpayers should understand before the problem escalates.

What Is Tax Debt?

Tax debt is any unpaid tax balance owed to the Internal Revenue Service or a state tax authority after a tax return is filed or a tax is assessed.

Tax debt may include:

- Unpaid federal or state income taxes

- Self-employment taxes

- Business or payroll taxes

- Penalties and interest added to unpaid balances

Once the payment deadline passes, the balance officially becomes tax debt and begins accruing interest and potential penalties.

How Tax Debt Commonly Starts

Most tax debt does not come from intentional wrongdoing. It often begins during financial transitions or unexpected life events.

Common causes include:

- Owing more than expected after filing a return

- Under-withholding from wages

- Self-employment income without estimated payments

- Unfiled or late-filed tax returns

- Business cash flow problems

- Unexpected income such as bonuses, crypto, or investment gains

Even taxpayers who file on time can end up with tax debt if the full balance is not paid by the due date.

How Tax Debt Grows Over Time

One of the most important things to understand about tax debt is how quickly it increases.

Once a balance is unpaid:

- Interest accrues daily

- Failure-to-pay penalties may apply monthly

- Additional penalties can apply for late filing or underpayment

Even a modest tax balance can grow significantly over time if no action is taken.

What Happens If Tax Debt Is Ignored?

Ignoring tax debt does not make it disappear.

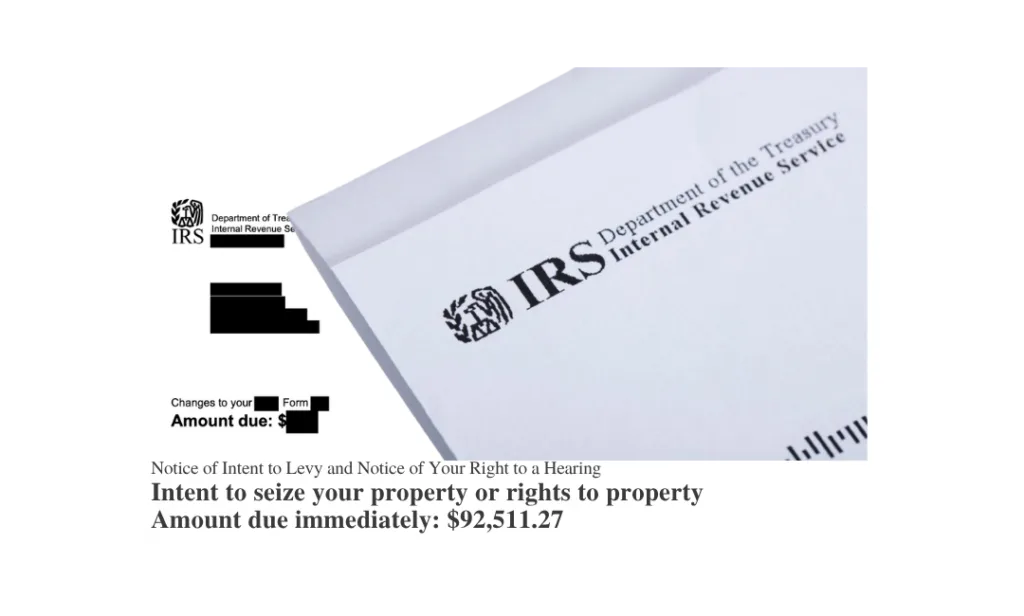

If no response is made, the IRS may escalate collection efforts, which can include:

- IRS notices and demand letters

- Federal tax liens

- Wage garnishments

- Bank levies

- Offset of future tax refunds

While the IRS usually begins with notices, enforcement actions become more likely the longer the balance remains unpaid.

How Long Does Tax Debt Stay With You?

The IRS generally has 10 years from the date a tax is assessed to collect the debt. This is known as the Collection Statute Expiration Date.

However, certain actions can pause or extend this timeline, including:

- Filing an Offer in Compromise

- Submitting appeals or collection due process requests

- Filing for bankruptcy

Relying on the statute alone without a plan can be risky, especially when enforcement actions are already underway.

When Tax Debt Becomes a Bigger Problem

Tax debt often becomes more serious when:

- Multiple tax years are involved

- Unfiled returns exist

- Business or payroll taxes are unpaid

- IRS enforcement actions have begun

At this stage, the issue is no longer just about payment. It becomes a compliance and resolution matter.

Why Addressing Tax Debt Early Matters

The IRS offers several resolution options depending on a taxpayer’s financial situation. These may include payment arrangements, temporary hardship status, or settlement programs.

Addressing tax debt early usually means more options, fewer penalties, and less risk of enforced collection.

Helpful Resources

- IRS: View Your Tax Account

- IRS Payment Options

- IRS Tax Topic 653: IRS Notices and Bills

- IRS Collection Process Overview

Frequently Asked Questions (FAQ)

Is tax debt a crime?

No. Owing taxes is not a crime. Tax debt only becomes a criminal matter in cases involving fraud, evasion, or intentional failure to file.

Can tax debt go away on its own?

No. Tax debt does not disappear unless it is paid, resolved, settled, or expires under the collection statute.

Does the IRS charge interest on tax debt?

Yes. Interest accrues daily on unpaid balances until the debt is resolved.

What happens if I can’t afford to pay my tax debt?

The IRS has programs for taxpayers who cannot pay in full, but eligibility depends on income, expenses, assets, and filing compliance.

Will the IRS take my paycheck if I owe taxes?

Wage garnishment is possible, but it usually happens only after multiple notices and a lack of response.

Does tax debt affect my credit score?

The IRS does not report tax debt to credit bureaus. However, federal tax liens filed before 2018 may still appear on credit reports.

Should I ignore IRS letters if I don’t have the money?

No. Responding early keeps more options available and reduces the risk of enforcement actions.

Can tax debt come from unfiled returns?

Yes. The IRS can assess tax based on its own estimates if returns are not filed, often resulting in higher balances.

Amro Badran, EA is the Managing Partner of BadranTax LLC,

Experienced and Trusted Tax Resolution Firm based in New Brunswick, NJ.

With over 40 years of experience and accreditation as a Federal Enrolled Agent, Amro Badran and his team of experts specialize in helping individuals and businesses resolve complex IRS issues and controversies.

Disclaimer

This blog post is provided for educational and informational purposes only.

It does not constitute tax, legal, accounting, or financial advice and should not be relied upon as a substitute for professional counseling tailored to your specific situation.

Always consult a qualified tax advisor or legal professional before making decisions based on this content.

Use of this site or information herein does not create a professional relationship between you and BadranTax LLC or its principals. Any reliance on the material is solely at your own risk.

While we strive to provide accurate, up-to-date information, BadranTax makes no warranties, express or implied, regarding accuracy, completeness, or suitability of the content.

Links to external websites are provided for convenience only. BadranTax does not endorse and is not responsible for the content or practices of third-party sites.

BadranTax and its affiliates expressly disclaim all liability for any actions taken or not taken based on this information.