If you paid IRS penalties or underpayment interest between 2020 and 2023 (Tax Years 2019-2022), a groundbreaking federal court case: Terry Kwong v. United States, means you may be legally entitled to a tax refund.

Millions of Americans received aggressive automated letters from the IRS during the pandemic.

Many taxpayers have searched for answers after receiving:

- IRS late filing penalties (Transaction Code 166)

- IRS late payment penalties (Transaction Code 276)

- Estimated tax underpayment penalties (Transaction Code 170)

- Federal Tax Deposit (FTD) penalties for businesses (Transaction Code 186)

- CP14 balance due notices and aggressive CP504 collection letters

- Accumulated penalty interest charges accrued during federal COVID relief periods

Thanks to a major court ruling, eligible individuals and business entities can now take active steps to recover those improperly assessed charges.

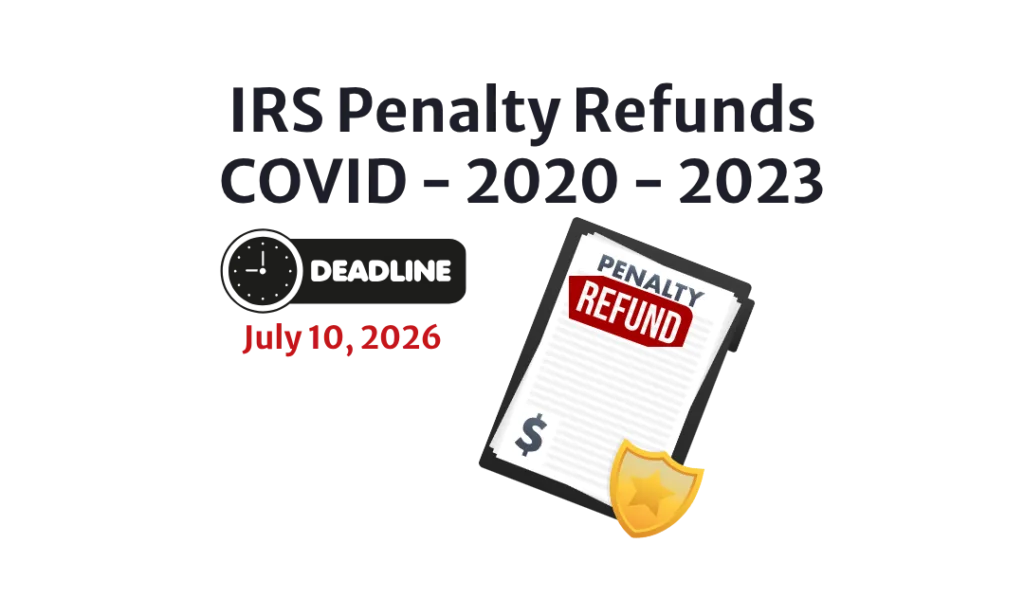

The absolute hard deadline to file a protective refund claim to preserve your money is July 10, 2026. With less than two months remaining, time is already running out.

What Is Kwong v. United States?

Kwong v. United States (Court of Federal Claims, No. 23-267 T) is a landmark federal tax lawsuit that redefines how IRS penalties and interest apply to the COVID-19 disaster relief window.

The core of the case hinges on Internal Revenue Code (IRC) § 7508A.

The court determined that when a federal disaster is declared, certain tax filing and payment deadlines are automatically postponed. Because the official COVID-19 national emergency period ran until May 11, 2023, the addition of the law’s mandatory 60-day extension tail pushed the legal due dates for tax returns back to July 10, 2023.

In her final ruling, Judge Molly R. Silfen clarified that standard tax returns for 2019, 2020, 2021, and 2022 were technically not “late” if they were handled during this relief window.

As a result, billions of dollars in IRS penalties and interest assessed prior to July 10, 2023, are arguably improper and eligible for a full refund or balance abatement.

This legal ruling impacts a massive audience, including:

- Individuals and self-employed 1099 taxpayers

- Small businesses, S Corporations, and Partnerships

- Trusts, estates, and non-profit organizations

Why This IRS Refund Issue Matters

(Even if You Still Owe Money)

The IRS has not, and will not, broadly issue automatic refunds for this issue. Taxpayers must proactively file administrative refund claims to protect their rights.

Importantly, this program is highly beneficial even if you currently owe an outstanding balance to the IRS. If your protective claim is successful, the IRS must strip away the improperly assessed penalties and interest from your account transcript, instantly slashing the total amount of principal debt you owe today.

Who Qualifies for an IRS Penalty Refund?

You may qualify for relief if you fit any of the following pandemic-era scenarios:

- You filed your federal tax returns late during 2020, 2021, 2022, or 2023.

- You were forced to pay your personal or corporate taxes late during the pandemic.

- Your business was hit with heavy Federal Tax Deposit (FTD) penalties or late-filed K-1/Information Return fees.

- You set up an IRS installment agreement or payment plan that piled on monthly penalties and compounding interest.

Calculate Your Potential COVID Refund Instantly

Curious if the IRS owes you money under the Kwong v. United States ruling?

Don’t sort through complicated tax transcripts or calculate interest tables blindly.

📊 Try Our Free IRS Penalty Relief Estimator

Launch the Free Penalty Estimator Tool →

By plugging in a few simple data points from your pandemic-era notices or records of what you paid, our digital estimator will calculate an rough approximate dollar recovery amount and verify whether Badran Tax’s professional program can step in to help you get your refund.

What IRS Notices Are Connected to These Penalties?

If you received any of these common IRS collection letters, you are a prime candidate for a Kwong review:

- CP14 – Official Notice of Balance Due

- CP501 / CP503 – Reminder and Urgent Balance Notices

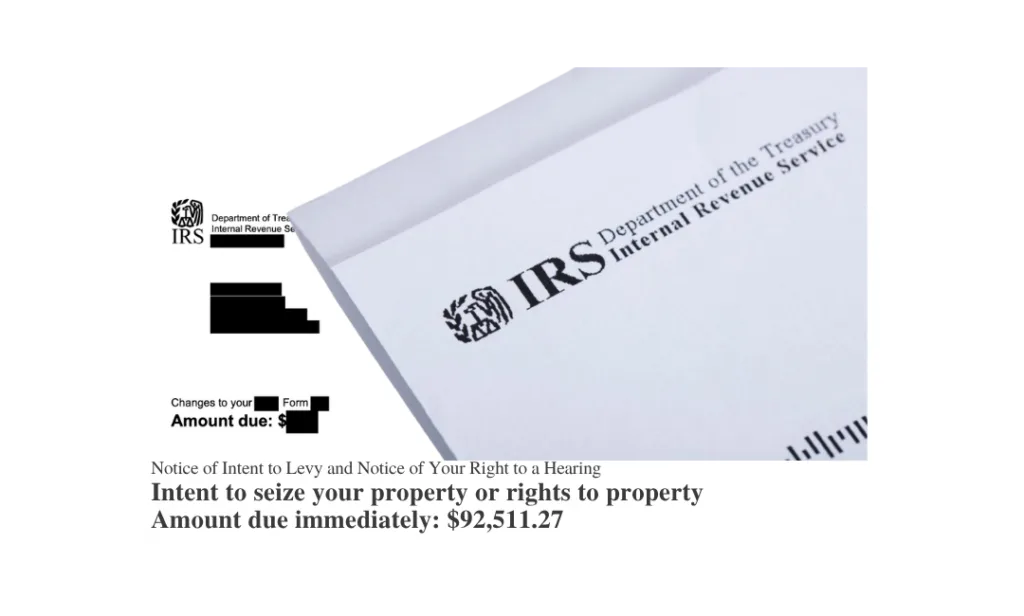

- CP504 – Notice of Intent to Levy (Asset Seizure Warning)

- LT11 or Letter 1058 – Final Notice of Intent to Levy and Right to a Hearing

Even if you long ago paid these balances off completely to clear your record, you maintain the legal right to demand that money back.

Refundable Penalty Types & Transaction Codes

| Penalty Type | IRS Transcript Code | The Legitimate Kwong Argument |

|---|---|---|

| Failure-to-File | Code 166 | Deadlines were automatically postponed by law, making returns filed before 7/10/2023 timely. |

| Failure-to-Pay | Code 276 | Late payment fees should not have been enforced while disaster statutory extensions were active. |

| Estimated Tax Penalty | Code 170 | Relief applies to underpaid quarterly estimates due during the disaster periods. |

| Federal Tax Deposit | Code 186 / 180 | Applies to corporate payroll tax deposit delays occurring during the relief windows. |

| Underpayment Interest | Code 190 / 196 | All interest accrued on unpaid tax balances prior to July 10, 2023, must be fully abated. |

What Is a Protective Refund Claim?

Because the federal government wants to prevent massive payouts, the Department of Justice officially filed a formal Notice of Appeal on May 15, 2026, trying to overturn the Kwong ruling.

This appeal means the IRS is currently holding or denying incoming claims while the higher courts review the case.

To protect yourself, you must file what is called a Protective Refund Claim using IRS Form 843. A protective claim locks in your place in line before the statute of limitations expires on July 10, 2026.

If the appellate courts uphold the original decision, only taxpayers who filed a valid protective claim before the deadline will secure their refunds. If you wait for the appeal to finish, your legal window to apply will be completely gone.

How Badran Tax Helps You Recover COVID-Era IRS Penalties

Preparing a compliant protective claim is a technical accounting process that requires specialized attention.

The tax experts at Badran Tax handle the heavy lifting for you:

- Secure Third-Party Authorization: We establish a secure Form 8821 or Form 2848 authorization to pull your official IRS master files without interrupting your day.

- Audit Transcript Histories: We trace every single Transaction Code (166, 276, 170, 186) across your 2019–2022 records.

- Precise Math Calculations: We calculate the exact dollar difference between what the IRS charged you and what is legally allowable under the Kwong extended timeline.

- Ironclad Submissions: We complete Form 843 with mandatory court references and submit via Certified Mail to establish undeniable proof of your timely filing.

Our experienced team consists of Enrolled Agents and seasoned tax resolution professionals equipped with specialized transcript auditing software to secure your family’s or business’s money back.

The July 10, 2026 Clock Is Ticking

Don’t let the IRS keep money that legally belongs to you.

Frequently Asked Questions (Expanded)

What inputs do I need to prepare for the Estimator tool?

To get the most accurate estimate, it helps to have your tax years (2019–2022) available, along with any balance-due letters (such as CP14 or CP504 notices).

If you don’t remember the exact numbers, you can input estimated ranges, and our software will calculate your potential refund tiers.

Has the government appealed the Kwong v. United States decision?

Yes. The Department of Justice formally filed a Notice of Appeal to the U.S. Court of Appeals for the Federal Circuit on May 15, 2026.

This ongoing litigation is precisely why filing a protective claim right now is vital. It secures your claim in line so that when the appeal concludes, your rights remain fully preserved.

What happens if I miss the July 10, 2026 filing deadline?

If you fail to file your Form 843 protective claim by July 10, 2026, the statutory three-year clock under IRC § 6511 expires completely for a significant portion of these pandemic years.

Even if the higher appellate courts eventually rule in favor of taxpayers, you will be legally barred from collecting a refund if your paperwork wasn’t stamped before this deadline.

Can corporate businesses and partnerships use this relief program?

Absolutely. In fact, corporate entities, S-Corps, and partnerships often have the highest dollar recoveries.

The Kwong postponement rules apply directly to late-filing fees for corporate information forms, missing K-1 generation penalties, and costly Federal Tax Deposit (FTD) penalties (Codes 186/180) triggered by pandemic liquidity crunches.

What if my original tax problem stems from a joint return, but we are now divorced?

If the penalties were assessed on a Married Filing Jointly (MFJ) return, both original spouses must sign the Form 843 recovery claim to request the abatement.

Badran Tax can guide you through the process of formatting joint claims, organizing split refund considerations, or handling filings for a deceased spouse (using Form 1310).

How does this differ from the old automatic penalty relief under Notice 2022-36?

IRS Notice 2022-36 was a limited, administrative action that only automatically abated failure-to-file penalties for 2019 and 2020 returns.

It completely excluded failure-to-pay penalties, estimated tax penalties, and underpayment interest. A Kwong claim captures all of those omitted charges across 2019, 2020, 2021, and 2022.

Does this court ruling provide refunds for state or local penalties?

No. The Kwong case was decided in the U.S. Court of Federal Claims and explicitly covers federal taxes overseen by the IRS.

State departments of revenue manage separate disaster statutes and are unaffected by this federal decision.

If the IRS rejects my protective claim due to the appeal, what happens next?

If the IRS issues a formal notice of disallowance while waiting on the appellate courts, that notice automatically initiates a standard two-year statutory window to file a formal refund suit.

This action legally cements your leverage while the overarching judicial dispute plays out in Washington.

Sources & Important Resources

- National Taxpayer Advocate Blog – Millions Eligible for Significant Disaster Refunds

- Taxpayer Advocate Service – Managing Protective Claims for Refund

- IRS Guidelines – About Form 843 Claims

Amro Badran, EA is the Managing Partner of BadranTax LLC,

Experienced and Trusted Tax Resolution Firm based in New Brunswick, NJ.

With over 40 years of experience and accreditation as a Federal Enrolled Agent, Amro Badran and his team of experts specialize in helping individuals and businesses resolve complex IRS issues and controversies.

Disclaimer

This blog post is provided for educational and informational purposes only.

It does not constitute tax, legal, accounting, or financial advice and should not be relied upon as a substitute for professional counseling tailored to your specific situation.

Always consult a qualified tax advisor or legal professional before making decisions based on this content.

Use of this site or information herein does not create a professional relationship between you and BadranTax LLC or its principals. Any reliance on the material is solely at your own risk.

While we strive to provide accurate, up-to-date information, BadranTax makes no warranties, express or implied, regarding accuracy, completeness, or suitability of the content.

Links to external websites are provided for convenience only. BadranTax does not endorse and is not responsible for the content or practices of third-party sites.

BadranTax and its affiliates expressly disclaim all liability for any actions taken or not taken based on this information.