Tax debt can feel like a heavy burden, affecting more than just your relationship with the IRS. It can have far-reaching consequences on your overall financial health, including your credit score, ability to obtain loans, and even your mental well-being. Understanding the broader implications of tax debt and taking steps to resolve it can significantly improve your financial stability and peace of mind. In this article, we’ll explore the impact of tax debt on your financial health and provide actionable strategies to fix it.

Credit Score and Financial Reputation

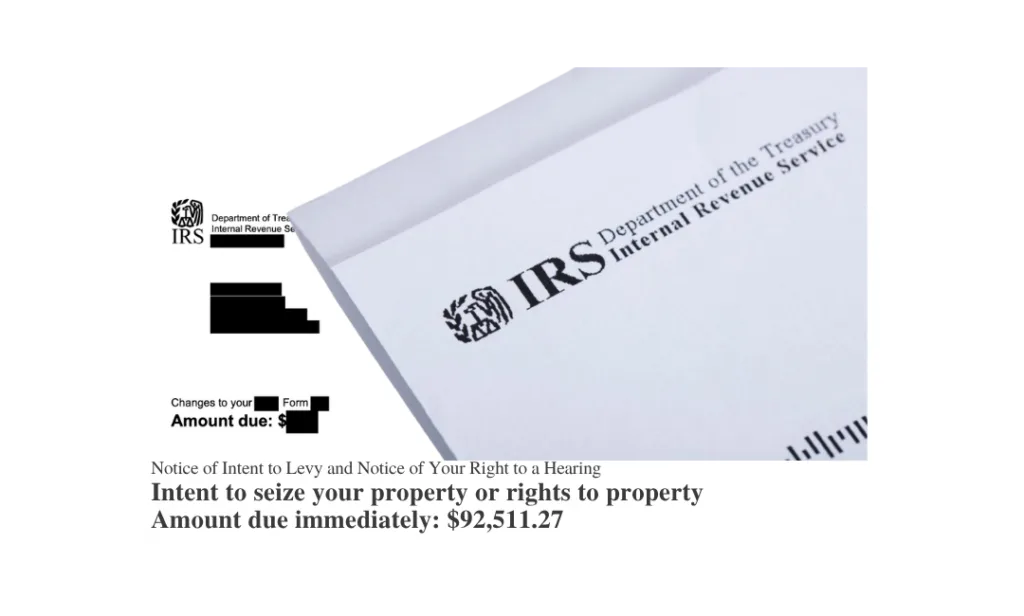

Unpaid tax debt can lead to the IRS filing a tax lien against you, which can severely damage your credit score. A tax lien is a legal claim against your property due to unpaid taxes, and once filed, it becomes public record. This can make it difficult to obtain credit, secure a mortgage, or even get approved for a rental property. The lien remains on your credit report for up to seven years, even after the debt is paid, affecting your financial reputation long-term.

Increased Financial Stress

The pressure of tax debt can lead to significant financial stress. This stress can manifest in various ways, from difficulty managing everyday expenses to anxiety about future financial stability. The fear of potential IRS actions, such as wage garnishment or asset seizure, can compound this stress, making it difficult to focus on other financial goals.

Limited Access to Loans and Credit

Tax debt can limit your access to loans and credit. Lenders view tax liens as a sign of financial instability, making them less likely to approve applications for personal loans, business loans, or credit cards. Even if you are approved, you may face higher interest rates and less favorable terms due to the perceived risk.

Potential for Increased Penalties and Interest

The longer your tax debt remains unpaid, the more it will grow due to penalties and interest. The IRS charges a failure-to-pay penalty of 0.5% of your unpaid taxes for each month you don’t pay, up to 25% of your total tax debt. Interest accrues daily on your unpaid balance, making it increasingly difficult to pay off the debt over time.

Resolving Tax Debt Is Possible & Can Improve Your Financial Health

Restoring Creditworthiness

By resolving your tax debt, you can remove tax liens from your credit report and begin to rebuild your credit score. This can open the door to better loan terms, lower interest rates, and greater financial opportunities. Paying off or settling your tax debt is the first step in restoring your creditworthiness and improving your financial reputation.

Reducing Financial Stress

Eliminating tax debt can significantly reduce financial stress, allowing you to focus on other financial goals like saving for retirement, buying a home, or investing in your future. With the threat of IRS actions lifted, you can regain control of your finances and enjoy greater peace of mind.

Avoiding Further Penalties and Interest

Addressing your tax debt promptly can help you avoid further penalties and interest, ultimately saving you money. The IRS offers several options for resolving tax debt, including installment agreements, offers in compromise, and penalty abatement, all of which can reduce the overall amount you owe and prevent the debt from growing.

Reclaiming Financial Freedom

Resolving tax debt frees you from the constant worry of IRS enforcement actions like wage garnishment or asset seizure. With your debt resolved, you can move forward with confidence, knowing that your financial future is secure.

How to Fix Your Tax Debt

1. Assess Your Tax Situation

The first step in fixing your tax debt is to assess your situation. Gather all relevant tax documents, including any IRS notices, and determine the total amount you owe. Understanding the full scope of your tax debt will help you decide on the best course of action.

2. Explore Your Resolution Options

The IRS offers several resolution options for taxpayers with outstanding debt:

- Installment Agreement: Allows you to pay off your tax debt in monthly installments over time.

- Offer in Compromise: Allows you to settle your tax debt for less than the full amount you owe if you can prove financial hardship.

- Currently Not Collectible Status: Temporarily delays IRS collection actions if you can demonstrate that paying your tax debt would cause financial hardship.

3. Seek Professional Help

Tax laws are complex, and navigating IRS procedures can be daunting. Seeking help from a tax professional, such as an Enrolled Agent, CPA, or tax attorney, can be invaluable. A professional can help you understand your options, negotiate with the IRS on your behalf, and develop a personalized strategy to resolve your tax debt.

4. Take Action Now

Once you’ve determined the best resolution option for your situation, take action promptly. The sooner you address your tax debt, the sooner you can begin repairing your financial health and moving forward with your life.

Conclusion

Tax debt can have a significant impact on your financial health, but it doesn’t have to define your financial future. By understanding the implications of tax debt and taking proactive steps to resolve it, you can restore your credit, reduce financial stress, and reclaim your financial freedom. At BadranTax, we specialize in helping clients navigate their tax debt and find effective solutions tailored to their needs.